Philip Shepherd, PwC Middle East Hospitality & Leisure Leader and Alison Grinnell, PwC Middle East Hotels Leader discuss the Middle East cities hotel forecast for 2015 and 2016.

Exponential growth

Growth fundamentals for the region’s hotel industry remain strong, with solid performance in terms of ADR (average daily rate) and occupancy levels; however, external factors present new challenges. The conflict between Russia and Ukraine combined with the oil price decline has led to the significant weakening of the Rouble. This plus the 25% devaluation of the Euro versus the dollar are impacting tourist numbers. We believe it may take time for this to reverse, so oversupply could become an issue, especially at the crowded luxury end of the market.

Growth fundamentals for the region’s hotel industry remain strong, with solid performance in terms of ADR (average daily rate) and occupancy levels; however, external factors present new challenges. The conflict between Russia and Ukraine combined with the oil price decline has led to the significant weakening of the Rouble. This plus the 25% devaluation of the Euro versus the dollar are impacting tourist numbers. We believe it may take time for this to reverse, so oversupply could become an issue, especially at the crowded luxury end of the market.

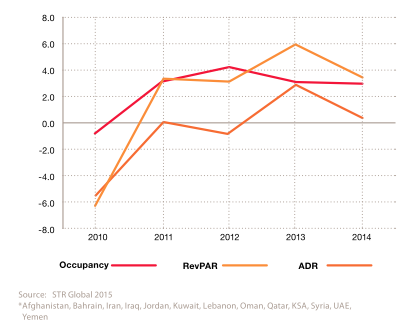

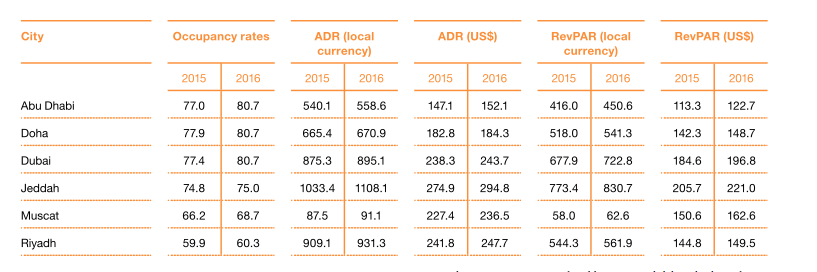

Our report looks at the prospects and key issues facing the hospitality industry in the featured cities of Dubai, Abu Dhabi, Doha, Jeddah, Muscat and Riyadh. All six cities saw an increase in RevPAR in 2014, with a double-digit rise in Doha, and nearly that in Jeddah. Abu Dhabi and Muscat saw around a 6% increase, and Dubai managed only marginal RevPAR growth as occupancies fell. By contrast, Riyadh saw occupancy gains of over 6% but ADR tumbled, so RevPAR rose only 1.1%.

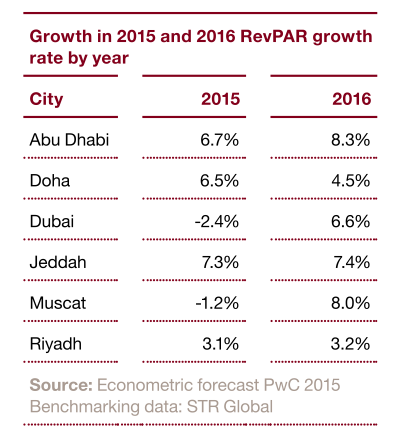

Our forecast for 2015 and 2016 paints a different picture; after a mixed year in 2015 where we believe growth will again be the dominant theme for 2016. The cities best placed for growth in 2015 are Jeddah and Abu Dhabi, with forecast RevPAR growth of 7.3% and 6.7% respectively, and growth also expected in Doha (6.5%). However, Muscat, Dubai and Riyadh are likely to see a decline in RevPAR.

In 2016, according to our findings, we see that there will be positive growth in all six cities. Muscat and Abu Dhabi are forecast to achieve good growth in both ADR and occupancy, driven by infrastructure spend, moderate supply increases, and the increase in tourist numbers that will result from Government promotional programmes. Doha is expected to see a return to positive ADR growth in both 2015 and 2016; however the city’s ability to manage the supply coming on board will be the driving factor to achieving this forecast.

In 2016, according to our findings, we see that there will be positive growth in all six cities. Muscat and Abu Dhabi are forecast to achieve good growth in both ADR and occupancy, driven by infrastructure spend, moderate supply increases, and the increase in tourist numbers that will result from Government promotional programmes. Doha is expected to see a return to positive ADR growth in both 2015 and 2016; however the city’s ability to manage the supply coming on board will be the driving factor to achieving this forecast.

The 25% devaluation of the Euro against the Dollar, has also led to a drop in visitors from the Eurozone. As a Dollar-based economy, the Middle East has now become a very expensive destination for those in the Eurozone, resulting in not only a drop in visitors from there, but also GCC nations heading to Europe for shopping tourism, rather than travelling within the Middle East region.

A need for leisure

The arrival of tourists from new markets calls for more leisure activities to be developed in the region as most of the tourist authorities in the region continue to expect visitor numbers to increase significantly, and most predict these new tourists will come from new markets, such as China, India, and elsewhere in Asia. The growth of the Muslim population in China will also lead to higher numbers of Chinese visiting the region, especially Mecca and Medina.

The challenge for the operators will be to understand and meet the needs of these new tourists, which tend to be different from those of Europeans or Russians. The Middle East needs to provide more leisure activities beyond the beach and the facilities available inside its hotels. Projects like Dubai Park & Resorts, the Angry Birds theme park in Doha, and the Louvre, Zayed National Museum, and Guggenheim projects in Abu Dhabi are already being planned and developed.

With the 6 billion people in reach of the UAE within 8 hours and the UAE landscape set to expand further with the addition of at least 5 full-scale theme parks in the next 3 years, if the UAE takes a holistic approach to its destination management, offering an Emirates-wide vision and coordination, encouraging collaboration and partnerships between all stakeholders, it can exploit its unique geographical location and deliver high quality attractions that can weather the diverse cultural requirements of the Middle East and the extreme summer weather conditions. This will put the UAE in direct competition with the likes of Singapore and Hong Kong in the east, mainland China and the ‘granddaddy’ of the sector, Orlando.

Risk of oversupply

High occupancy has been a long-term trend in the region, but with so much new supply coming on-stream, there lies to be a question mark about whether this is sustainable in the future. With over 54,000 rooms under construction and another 72,000 planned for the region, supply could well start to outstrip demand, putting ever-greater pressure on both occupancy and ADR.

Interestingly, we have seen that during the peak month of February 2015, regional supply exceeded demand in a peak time for the first time since in 2009. We expect supply to exceed demand in the summer months, however in peak times this is a more worrying trend.

Interestingly, we have seen that during the peak month of February 2015, regional supply exceeded demand in a peak time for the first time since in 2009. We expect supply to exceed demand in the summer months, however in peak times this is a more worrying trend.

Reassessing the right mix of hotels

The oversupply of the luxury end of the market and the change in the profile of tourists coming to the region are calling for a reassessment of the type of hotels available to tourists.

One of the many anomalies about the Middle East’s hotel sector is the high number of hotels in the five star and luxury segment. Most mature markets would have a more even distribution or a ‘pyramid’ distribution of properties, with the majority in economy or budget, and fewer at the ultra-premium end.

In the Middle East, this pattern is inverted, with huge numbers of luxury rooms, especially in Dubai – at present, around 10,000 rooms are in construction in Dubai, of which less than 1,000 are in the mid-range or economy segment.

Online agencies change the face of hospitality

Digital now dominates the way people manage their travel, as they use sites to find and book flights and accommodation and use social media to feedback their experiences. There’s no question that this have benefited many hotels, however over time, this has been counterbalanced by the challenges this ‘digital disintermediation’ brings.

Our findings show one thing that hasn’t changed is the management contract between the owner and operator. Given that so much of the hotel’s reputation is now determined online, we query whether management contracts need to find a way to reward – or sanction – operator’s performance in this area.

{kind=link}