As the global economy recovers, investment sentiment is on the up, with strong demand for proven destinations in America, Europe and the Middle East, Sarah McCay reports

Global hotel investment is on the up in terms of short and medium term sentiment, according to the latest Hotel Investor Sentiment Survey, published by JLL in December 2014.

According to the property services firm, investors’ near-term sentiment for trading globally increased over the last six months of 2014, with investor short-term expectations up 5.4 percentage points to 63.2%, while medium-term sentiment softened by a modest 5.5 percentage points to 61.1%.

Data from the survey showed that market fundamentals remained strong as access to capital continued to improve, with markets that had been less active witnessing increased activity.

Major gateways ranked highest for short-term trading at 68.8% followed by EMEA at 65.6%. Over the medium-term, investors favour hotel markets in EMEA at 72.9% and major gateways at 65.9%.

“Key gateway cities in the Americas and Europe, such as New York, Paris, London and Rome, remain the most attractive hotel investment markets. In the Middle East, Dubai remains at the top of the investors’ wish list, followed by Abu Dhabi then core markets in Saudi Arabia, although the latter markets are more in terms of development than operating hotel transactions,” says Chiheb Ben Mahmoud, executive vice president – head of hotels & hospitality, Middle East & Africa, JLL Hotels & Hospitality Group.

In terms of transactions, ‘hotel investments’ in the JLL report refer mostly to deals on existing assets rather than the development of new hotels. Despite this, the Middle East region still continues to show strong potential, as investors are wooed not only by the amazing blueprints of hotels yet to be, but also by some of the existing landmark property coming to market in the region.

Globally, JLL cites that investors’ primary strategy over the next six months is acquisition at 40.3%, disposal at 31.1% and development at 28.3%.

“In terms of transactions, Chinese investors have a strong preference for real estate assets including hotels. It is expected that they will continue to be behind significant and landmark transactions whether in traditional markets of proximity, such as Asia Pacific, or in more remote and complex markets such as Western Europe,” explains Ben Mahmoud.

“In terms of developments, all emerging destinations in the Middle East and Africa region will continue to increase the size of their hotel supply albeit at different paces among still relatively constrained hotel financing,” he adds.

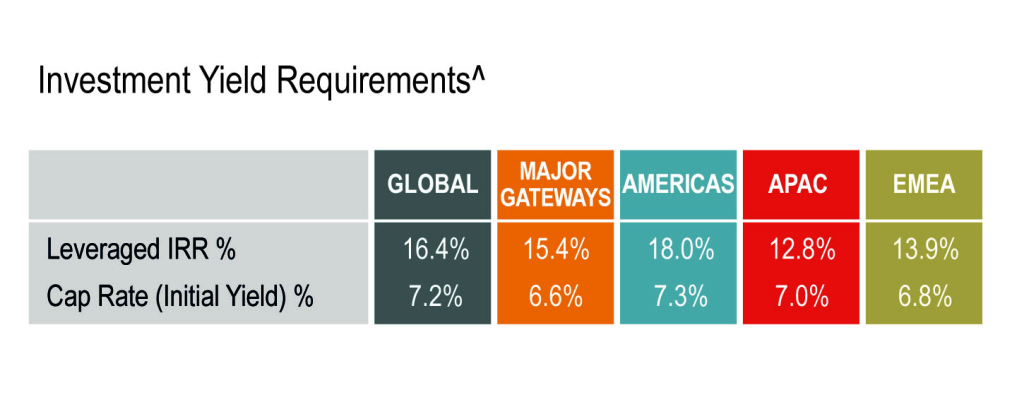

According to JLL, investor expectations for global leveraged internal rates of return (IRRs) recorded a 130 basis point increase to 16.4% in 2014. Regional leveraged IRR expectations were lowest for Asia Pacific at 12.8% and highest for the Americas at 18%.

Global cap rate expectations recorded a 10 basis point bump averaging 7.2%. Cap rate expectations were lowest for the major gateways at 6.6% and EMEA at 6.8%. Investors expect global cap rates to contract slightly over the next six months with the downward trend most evident in the Americas.

Americas

While cap rates may be contracting, investor sentiment remains optimistic across North America with regards to hotel investments, with investors’ hotel performance sentiment also improved during 2014.

The positive push follows improved economic news for North America, with quantitative easing and the recession now history. Hotel performance is mirroring that of the national economy, with steady growth being witnessed.

Of the top-25 US markets, 21 have reached their pre-recession revenue per available room (RevPAR) peaks. Driven by more positive hotel operating profits, hotel investors have a resoundingly positive outlook for continued lodging sector growth.

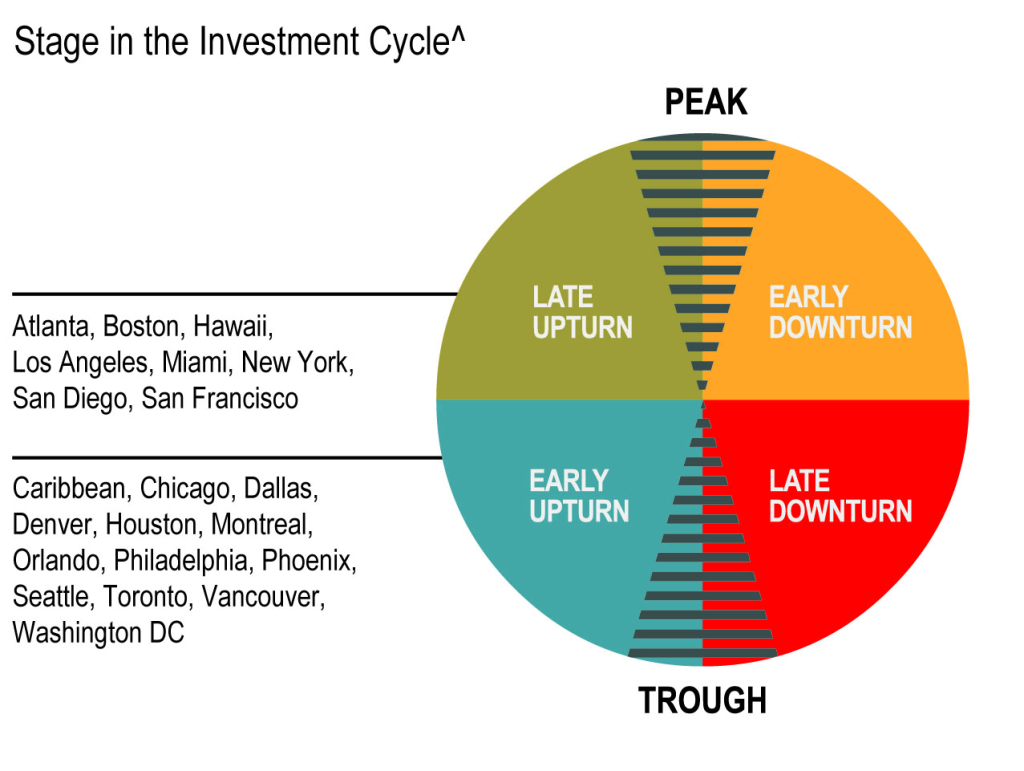

Looking ahead to performance for the first half of 2015, the JLL Hotel Investor Sentiment Survey tipped San Francisco, Seattle and Houston as destinations to watch. In the two-year timeframe the Caribbean ranked highest, followed by Los Angeles, Vancouver and San Francisco.

In Canada, Vancouver’s medium-term performance outlook is most encouraging, followed by Toronto and Montreal, respectively. Vancouver and Toronto garnered among the highest medium-term performance expectations in the Americas.

Of the investors surveyed by JLL, 46% of respondents are primarily pursuing acquisitions, while 31% are focusing on selling assets. As such, transaction levels are expected to increase across North America, with 2014 figures expected to close at US$25 billion, marking a six-year high.

Some 23% of investors cited development as their main strategy looking forward, an increase of one percentage point on a year previous. Development intentions are highest in Boston, San Francisco and Seattle and lowest in Phoenix, Orlando and Atlanta. Branded mid-market hotels will make up the majority of new inventory as upscale select service properties comprise 60% of the region’s active pipeline.

EMEA

The Europe, Middle East and Africa (EMEA) region presents a mixed bag of fortunes and sentiment for hotel investors, swayed largely by recession in some Eurozone countries.

In general, short-term trading expectations across EMEA reported a slight uptick since April 2014, rising 10 basis points to 65.6%, while investor sentiment for the medium term softened slightly falling 60 basis points to 72.9%.

“The opportunities vary from one country to another in the EMEA region and even in some instances within the same country across destinations. For example, in Spain there is a difference between Madrid and Costa del Sol. In general, opportunities are ‘less obvious’ and require sophisticated buyers with a proactive and clear strategy. In the Middle East, opportunities do exist for investors with reasonable yield expectations and a clear strategic focus,” advises JLL’s Ben Mahmoud.

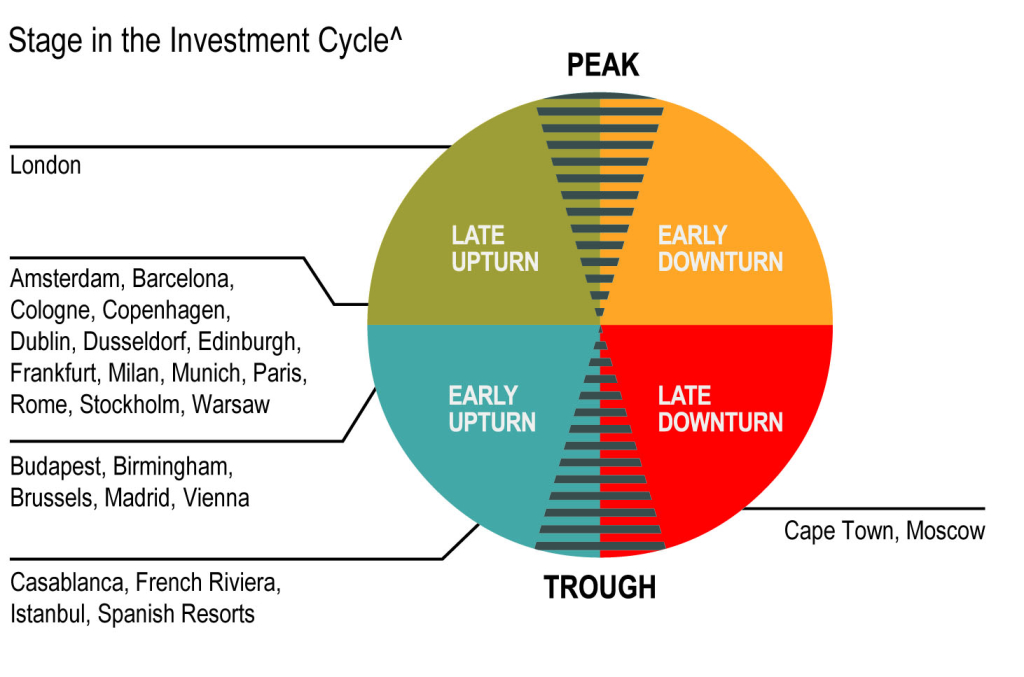

Of the 32 cities tracked, short-term expectations are highest for Copenhagen, London, Stockholm and Warsaw. Looking further ahead, medium-term sentiment is strongest in Dubai, Casablanca, Amsterdam and Paris.

According to JLL, short-term expectations for Copenhagen are robust at 100%, falling to 69.2% over the medium term. The Danish capital reported some of the strongest RevPAR growth October 2014 YTD according to STR Global, up 15.5% driven by strong ADR growth.

In the UK, trading expectations remained strong for London in both the short and medium term. International visitor arrivals during the first six months of 2014 rose 7.6% to nearly 8.5 million trips compared to the same time in 2013, leading to a strong first half for the capital’s hotels.

The outlook throughout the rest of the UK is also promising, with strong trading expectations in both Edinburgh and Manchester. Manchester is the UK’s third most visited city and boasts extensive conference and event facilities, major sporting stadia and the largest museum and theatre sectors outside London.

In the Middle East, investor sentiment is high for Dubai with a positive net balance of 86.7%. While developers are optimistic about building in Dubai, with more than 21,000 hotel rooms and serviced apartments expected to enter the market by the end of 2017 in the luxury sector, attaining Dubai’s goal of attracting 20 million visitors by 2020 will require the emirate to also increase its midscale offering, which is slightly les appealing to investors.

There is also concern about where these extra visitors will come from. Dubai relies heavily on the Russian market, but with the depreciation of the rouble and political uncertainty, the number of visitors is expected to fall and it will be necessary to attract visitors from new feeder markets if the emirate is to achieve this goal.

“Dubai attracts investors, not because of the requirement of rooms, which would tend to act in the opposite direction as there would be expectation of larger supply, but because of three main reasons: (1) the unique infrastructure; (2) the track record of the entire tourism chain, including retail, entertainment etc., in delivering a complete and co-ordinated experience; and (3) continued and consistent focus on tourism as a strategic development driver,” says Ben Mahmoud.

However, he is quick to add that opportunities do exist elsewhere, whether in North Africa or Sub Saharan Africa, in Oman, or in the Indian Ocean.

Investors into the EMEA are now pushing for better returns as many of the markets report business gains. The JLL survey showed that expectations for leveraged IRR requirements currently sit at 14.2%. This places IRR requirements 130 basis points lower than the long-term average of 15.5% and shows that investors are seeking higher returns on their investments than they were six months ago.

It could be argued that the Middle East investor is central to this, as funds from Qatar, Kuwait and the UAE continue to buy up prime hotel assets across the region, and not just in their domestic markets.

“The Middle East region continues to be a net buyer of hotel assets vis-à-vis the rest of the world; there are more Middle Eastern investors acquiring hotels abroad than foreign investors buying in Dubai,” explains Ben Mahmoud.

“As a general rule, hotel development tends to be a local play. Sometimes you have capital inflow for strategic purposes, hotel or non-hotel related,” he adds.

According to the survey results, investment funds and private equity groups are the most acquisitive groups currently targeting EMEA hotel real estate, followed by banks and institutional investors.

“Hotels have emerged over the last few years as a real estate asset class attracting the interest of a larger pool of potential investors and they have showed a fair level of resilience,” Ben Mahmoud comments.

Talking about the main buyer and seller types being seen in the Middle East, he says: “The players cover a wide range – local, regional and international investors with the locals from Dubai, Abu Dhabi and other Emirates taking the leading share. Although there is a strong interest from a large pool of international investors who continue to scan the market, the main buyers are from the region. In line with the existing ownership structure, sellers are obviously from the region.”

Asia Pacific

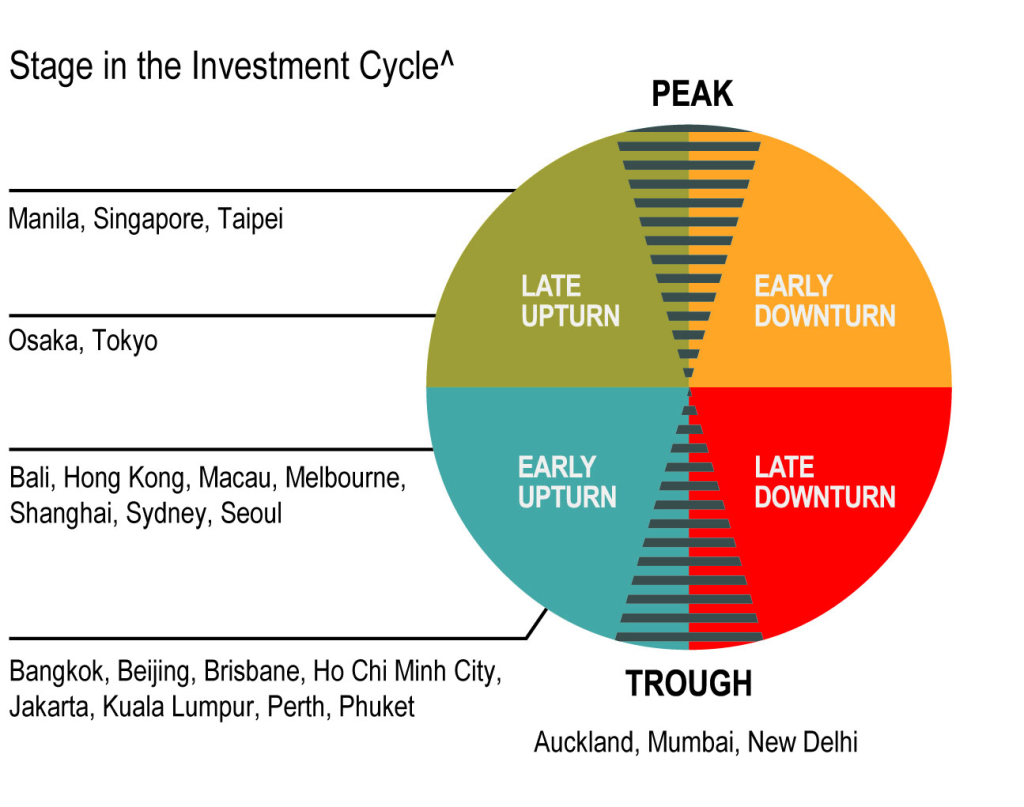

Investor sentiment for trading in Asia Pacific hotel markets increased substantially during the second half of 2014, with short-term expectations surging to 63.5% and medium term increasing to 56.3%.

Investor expectations for leveraged IRRs fell slightly, averaging 12.8%, with higher expectations for Australasian assets, which increased to 12% from 10.8% in April 2014, stated JLL. This was offset by a slight reduction in expectations for Asia, reflecting the premium that is being channelled to the large volume of capital chasing hotel assets.

However, Asia Pacific cap rate expectations tightened further as outbound capital continued to chase hotels with new entrants attracted to the sector and few assets available for sale. Cap rate expectations tightened by a respectable 20 basis points to average 7%.

Divergent cap rates are expected over the next six months across Asia Pacific but further rate compression is anticipated in Brisbane, Ho Chi Minh City, Jakarta, Kuala Lumpur, Manila, Osaka, Phuket, Singapore, Sydney and Tokyo.

“Investors should watch all of Asia Pacific. Malaysia is a champion, which has been negatively impacted over the past few months by travel related bad news, while Thailand had some stability challenges. However, Asia Pacific is otherwise a very deep region in term of hotel investment opportunities and that includes destinations such as Australia and Vietnam,” points out Ben Mahmoud.

A new ruling set by the Chinese Ministry of Commerce (MOC) came into effect on 6 October 2014. Under the previous rules, any overseas investment project worth more than US$100 million required MOC approval. This requirement has now been abolished and is set to further increase outbound investment for hotel assets abroad.

2015 could prove an interesting year for hotel investment, especially with falling oil prices expected to lead to falling flight prices, encouraging even more travellers abroad, pushing hotel revPAR and ADR’s ever upwards.

{kind=link}